A Growing Share of Americans are Burdened by Housing Costs

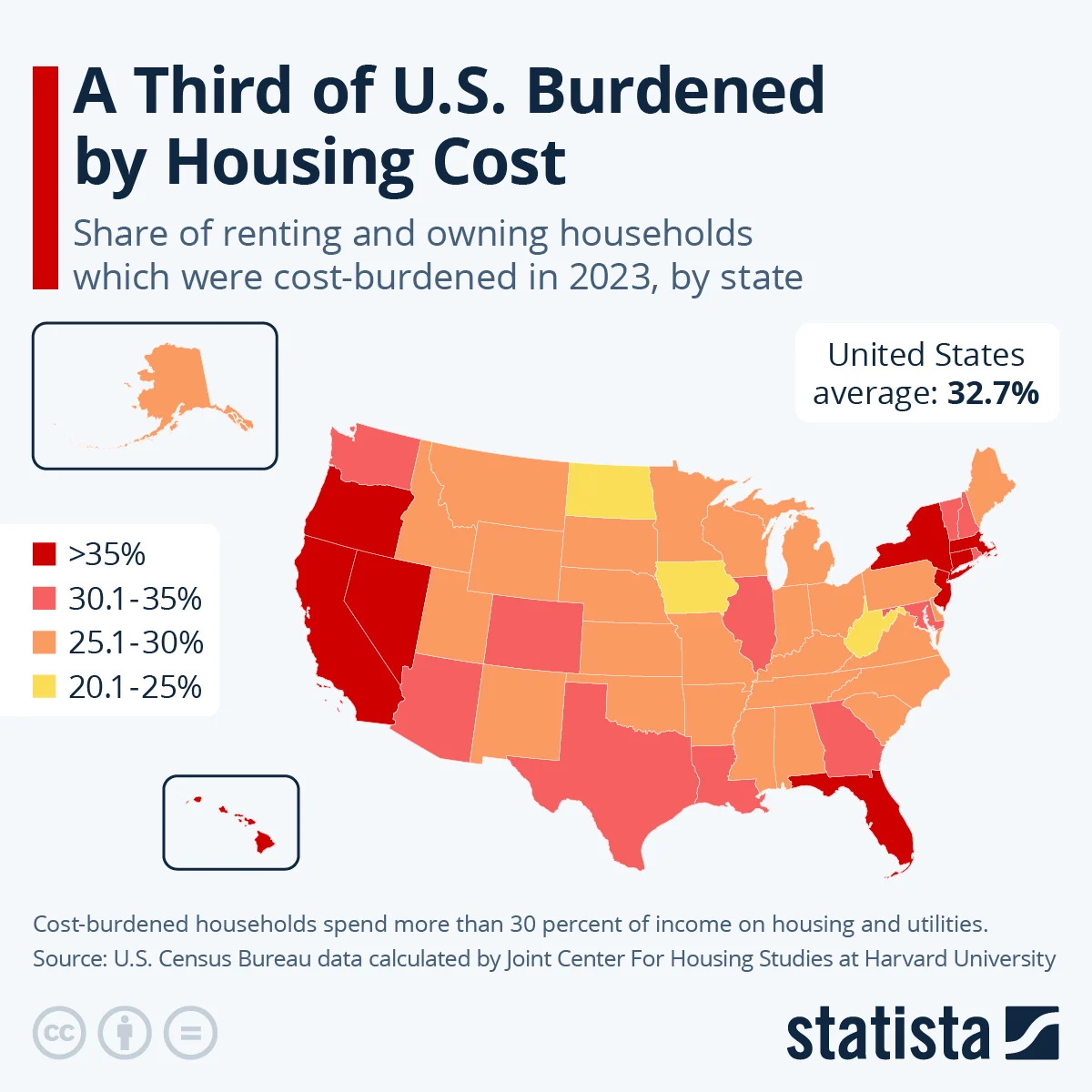

The housing affordability crisis isn’t exactly news, but it is getting worse. New data from Harvard’s Joint Center for Housing Studies shows that nearly one-third of all U.S. households are now officially “cost burdened.”

By Austin Payne

/

Published 7.22.2025

The housing affordability crisis isn’t exactly news, but it is getting worse. New data from Harvard’s Joint Center for Housing Studies shows that nearly one-third of all U.S. households are now officially “cost burdened.” That means they’re spending more than 30% of their income on housing and utilities, the threshold where financial stress tends to set in.

The burden isn’t evenly geographically distributed. In California, 42% of households are cost-burdened. It’s 40% in Hawaii, 39% in Florida, and 38% in New York. Meanwhile, in states like West Virginia, North Dakota, and Iowa, fewer than 1 in 4 households face that level of strain.

For years, renters were more likely to be financially stretched, but that gap started shrinking after 2022, when mortgage rates jumped, home prices stayed elevated, and insurance premiums and property taxes piled on new costs for homeowners.

And the broader affordability math is still ugly. As we reported last month, the median sale price for a U.S. home hit $396,500, with a median asking price of $422,238. The typical monthly mortgage payment remains close to its all-time high, at $2,820. Even those in a position to buy are thinking twice: Gallup’s latest polling shows that just 26% of Americans believe it’s a good time to buy a house — the lowest reading ever recorded, even worse than the 2008 housing crisis.

The root issue here is simple. Home prices are up 29% since 2019, far outpacing wage growth. The price-to-income ratio is now 5.0 nationally, compared to 4.1 pre-pandemic and 3.2 in the 1990s. Back in the 1980s, the median home cost 3.6x the median household income. Today, it’s 5.3x. Even with inventory rising — listings are up 14.5% year over year — the market remains gridlocked. Boomers aging in place, sky-high mortgage rates, and a growing mismatch between supply and what people can actually afford are all keeping pressure on prices.

Harvard’s report also warns of more stress ahead in the form of rising climate-related insurance costs, growing property taxes, and shrinking federal housing assistance. Combine that with a surge in homelessness and record-low homebuying activity, and the picture for 2025 and beyond looks…bleak.